East of Suez Market Update 19 Nov 2025

Prices in East of Suez ports have moved in mixed directions, and bunkering in Zhoushan’s OPL area remains suspended due to bad weather since 8 November.

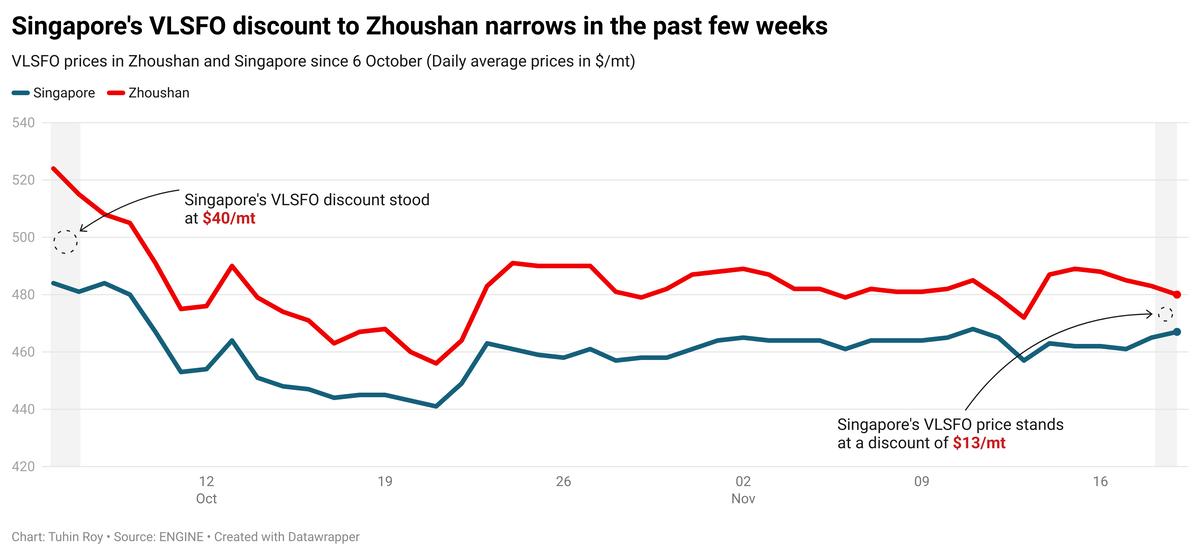

Changes on the day to 17.00 SGT (09.00 GMT) today:

- VLSFO prices up in Singapore and Fujairah ($5/mt), and down in Zhoushan ($3/mt)

- LSMGO prices up in Zhoushan ($9/mt), Fujairah ($7/mt) and Singapore ($2/mt)

- HSFO prices down in Zhoushan ($10/mt), Singapore ($6/mt) and Fujairah ($3/mt)

- B30-VLSFO at a $241/mt premium over VLSFO in Singapore

- B30-VLSFO at a $264/mt premium over VLSFO in Fujairah

Singapore and Fujairah have seen a slight rise in VLSFO prices over the past day, while Zhoushan's benchmark has dipped slightly. Singapore’s VLSFO is at a $7/mt premium over Fujairah and at a $13/mt discount to Zhoushan.

Delivery times for VLSFO are still uneven across suppliers in Singapore — ranging between 2-10 days — though this is marginally better than last week’s range of 3-12 days.

HSFO availability has improved, with lead times shortening to 5–10 days from 7–12 days. LSMGO supply has also strengthened, now requiring 2–8 days for delivery, compared with 3–10 days last week.

Demand in Zhoushan continues to be weak. VLSFO lead-time guidance remains at 4–6 days, and LSMGO stays unchanged at 4–6 days. HSFO, however, has lengthened slightly to 5–7 days from 4–6 days last week.

Adverse weather conditions have disrupted bunkering. Operations at the Tiaozhoumen and Xiazhimen outer anchorages have been shut since 8 November, according to a source. Bunkering resumed this morning at the more sheltered Xiushandong anchorage after being suspended since 10 November; it briefly opened over the weekend before closing again. The inner Mazhi anchorage remains fully operational, and suppliers expect all Zhoushan anchorages to return to normal tomorrow.

Brent

The front-month ICE Brent contract has gained by $0.48/bbl on the day, to trade at $64.37/bbl at 17.00 SGT (09.00 GMT) today.

Upward pressure:

Oil prices have risen as supply risks have emerged as the dominant driver of the global oil market.

The European Union’s (EU) renewed hardline stance on Russia has revived concerns about the possibility of tighter sanctions on the OPEC+ group.

Top EU diplomat Kaja Kallas remarked yesterday that Moscow’s aggression against the EU, including an explosion in Poland, should be treated as terrorism, Bloomberg reported.

Poland's Prime Minister Donald Tusk said on Tuesday that foreign intelligence services orchestrated an explosion on a railway line used to transport aid to Ukraine. Later, spokesman Jacek Dobrzynski said that "everything points to them being Russian special services", according to a BBC report.

“Language markets interpreted [Kallas’ comments] as raising the odds of further sanctions,” VANDA Insights’ founder Vandana Hari said.

These remarks come as the US sanctions on Russia’s two largest oil producers – Lukoil and Rosneft – are set to take effect shortly.

“Market participants appear more concerned about supply risks than the odds of a surplus going forward,” two analysts from ING Bank remarked.

Downward pressure:

The latest crude stocks report by the American Petroleum Institute (API) has put some downward pressure on Brent’s price today.

US crude oil inventories gained by 4.4 million bbls in the week ending 14 November, according to the API.

This was the third straight weekly build in inventories. A build in US crude stocks typically indicates lower demand for oil and can put downward pressure on Brent.

“The market will be more focused on the release of the widely followed US Energy Information Administration (EIA) inventory numbers later today,” ING Bank’s analysts said.

By Tuhin Roy and Aparupa Mazumder

Please get in touch with comments or additional info to news@engine.online