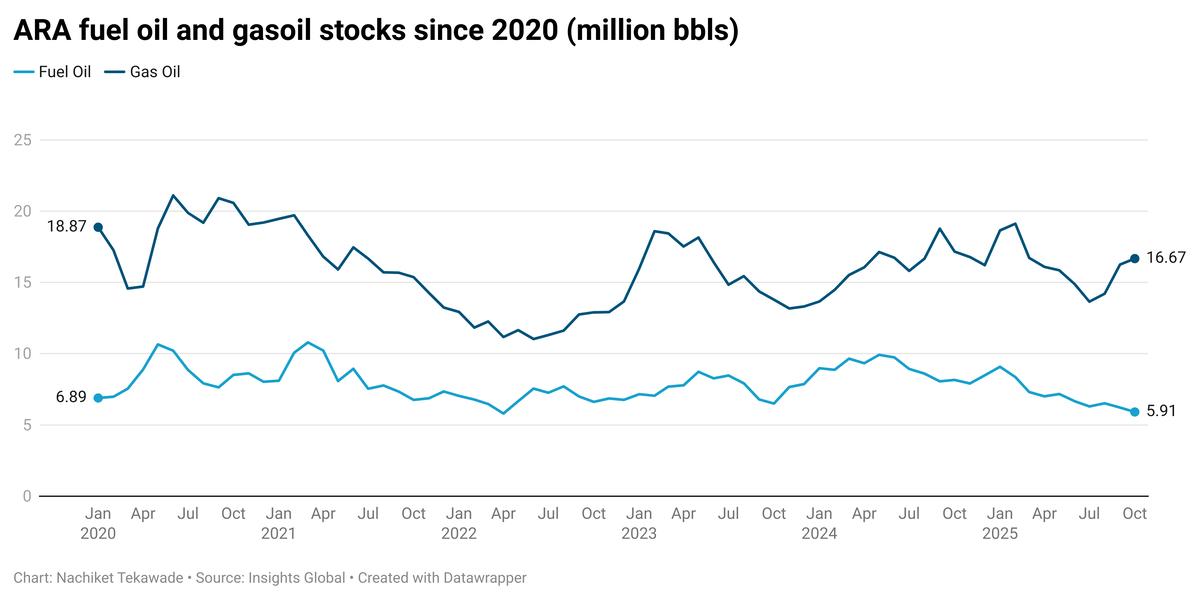

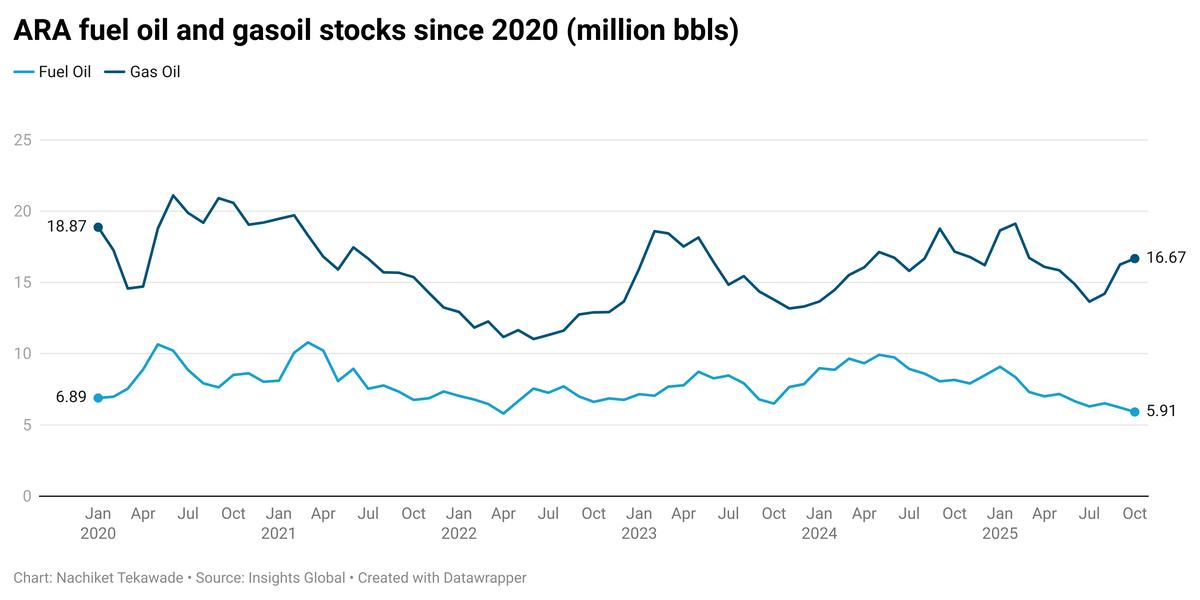

Europe & Africa Market Update 5 Nov 2025

Regional bunker benchmarks have moved in mixed directions, while prompt supply remains tight in the Gibraltar Strait.

IMAGE: Aerial view of the Bay of Gibraltar. Getty Images

IMAGE: Aerial view of the Bay of Gibraltar. Getty Images

Changes on the day to 09.00 GMT today:

- VLSFO prices up in Durban ($4/mt), Gibraltar ($2/mt) and down in Rotterdam ($5/mt)

- LSMGO prices up in Gibraltar ($6/mt), and down in Rotterdam ($9/mt)

- HSFO prices up in Durban ($3/mt), and down in Rotterdam and Gibraltar ($2/mt)

- Rotterdam B30-VLSFO premium over VLSFO up by $13/mt to $276/mt

- Gibraltar B30-VLSFO premium over VLSFO down by $4/mt to $336/mt

Among the conventional fuel prices at the three ports, Rotterdam’s LSMGO price has seen the steepest fall. A lower-priced 50-150 mt LSMGO stem fixed at $684/mt in the port has contributed to pull the benchmark down.

Meanwhile, Gibraltar’s LSMGO price has increased some in the past day. This has widened Gibraltar’s price premium over Rotterdam by $15/mt in a single session.

Securing prompt bunker deliveries can be difficult in Gibraltar. Lead times of around seven days are recommended for LSMGO and VLSFO, while HSFO deliveries may need a longer notice of more than two weeks, a trader told ENGINE.

Fifty vessels are expected to arrive for bunkers in Gibraltar between 6-13 November, shipping agent A. Mateos & Sons said.

Most suppliers in Gibraltar continue to be delayed by around 4-8 hours, while in the adjacent Algeciras port, some suppliers are operating almost a day behind schedule, port agent MH Bland said.

Easterly wind gusts of more than 25 knots and waves of over 2 metres are forecast in Gibraltar, Algeciras and Ceuta on 12 November, which could complicate bunker deliveries.

Brent

The front-month ICE Brent contract has gained by $0.45/bbl on the day, to trade at $64.56/bbl at 09.00 GMT.

Upward pressure:

Recent sanctions on Russia’s energy sector have supported Brent’s price this week.

The US Treasury Department’s Office of Foreign Assets Control (OFAC) had sanctioned Rosneft and Lukoil along with 34 of their subsidiaries in October.

Lukoil and Rosneft are Russia’s two biggest oil producers, according to market analysts. The sanctions have helped ease some market concerns about a potential supply glut anticipated in 2026.

“Given recent US sanctions on Russia, there is plenty of uncertainty as to the size of this surplus,” two analysts from ING Bank said. “If these sanctions disrupt Russian oil flows, it will eat into the expected surplus early next year,” they added.

Downward pressure:

Brent’s price has come under some downward pressure after the American Petroleum Institute (API) reported a sizeable increase in US crude stocks.

US crude oil inventories gained by 6.5 million bbls in the week ending 31 October, according to API estimates.

A build in US crude stocks typically indicates lower demand for oil and can cap Brent's price gains.

“Downward pressure [on Brent] continued in early morning trading today, following a bearish inventory report from the American Petroleum Institute (API),” ING Bank’s analysts noted.

The widely watched official data from the US Energy Information Administration (EIA) is scheduled for release later today.

By Nachiket Tekawade & Aparupa Mazumder

Please get in touch with comments or additional info to news@engine.online