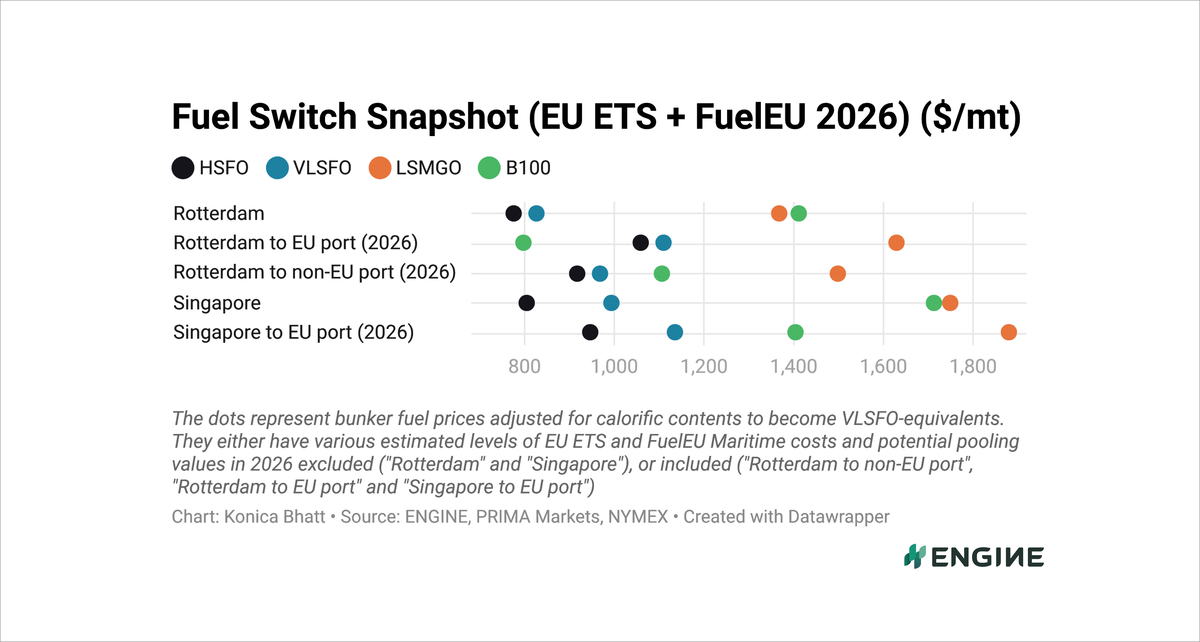

Fuel Switch Snapshot: B100 swings to discount to LBM with high-methane slip

B100 flips to a discount to LBM for Otto MS engines

Rotterdam B100’s discount to LSMGO crosses $800/mt

LNG-LBM spread in Rotterdam narrows for third week

Rotterdam’s B100 has switched to a discount to 0 gCO2e liquefied biomethane (LBM) consumed in Otto medium speed (Otto MS) engines for the first time since December.

LBM's high FuelEU Maritime pooling value has significantly reduced its effective cost since the regulation was implemented last year. This made it the most attractive compliance option for dual-fuel vessels in Rotterdam, regardless of whether these vessels had Otto MS or diesel slow speed (diesel SS) engines.

B100 has been at a consistent premium over LBM burnt in Otto MS engines from December until this week. One of the reasons for B100 costs falling relative to LBM has been a lower estimated FuelEU Maritime pooling value for both fuels. LBM generates a greater FuelEU compliance surplus and has taken the biggest absolute hit from a lower surplus price.

LBM's estimated FuelEU Maritime pooling value was $940-1,100/mt at the start of December and has now dropped by $80-90/mt to $860-1,010/mt. B100's estimated pooling value has dropped by a smaller $60/mt to $620/mt.

B100-LBM spreads have narrowed significantly over the past month, especially for for vessels burning LBM in high-methane-slip Otto MS engines. A sharp rise in LBM prices has contributed to flip LBM consumed in an Otto MS engine to a $76/mt premium over B100.

Rotterdam's LBM retains an edge for vessels with diesel SS engines, but its discount to B100 has narrowed by $114/mt on the week to $125/mt.

It should be noted that B100 and LBM largely cater to different vessel segments with distinct operational needs and fuel requirements, and do not necessarily compete with each other.

Rotterdam B100’s discount to LSMGO has widened by $204/mt to $832/mt in the past week. Its discounts to LNG have expanded by $72–74/mt, to $231–427/mt, depending on LNG engine.

Liquid fuels

Rotterdam’s HSFO and VLSFO prices have risen by $28-48/mt over the past week. A $74/mt rally in front-month ICE Brent futures has added upward pressure, while improved bunker fuel availability in the ARA hub could have capped sharper gains.

LSMGO has surged $244/mt higher, largely tracking a $274/mt jump in ICE low-sulphur gasoil futures.

Rotterdam’s B100 benchmark has gained $40/mt. Counter-pressure has come from an €11/mtCO2e increase in Dutch ZRE A ticket prices, which are now at €137–139/mtCO2e.

In contrast, Singapore’s conventional bunker fuel prices have declined by $19-153/mt, while its B100 benchmark has edged $3/mt lower.

B100’s premium over VLSFO in Singapore has widened by $150/mt, while its discount to LSMGO has narrowed by $17/mt.

Liquid gases

Rotterdam’s LNG bunker prices have climbed $111–114/mt higher, depending on methane slip. They have been supported by a 16% rise in the assessed LNG bunker premium, from $136/mt to $157/mt. Prices have been further underpinned by a sharp 14% gain in the front-month Dutch TTF natural gas contract.

Higher withdrawals from underground gas storage and growing fears of prolonged global LNG supply disruptions following damage to Qatar’s Ras Laffan gas field have pushed TTF upwards.

“The impact [of Ras Laffan damage] is likely to be long term, with restoration of production expected to take more than three years,” ANZ Bank senior commodity strategist Daniel Hynes said.

Rotterdam’s LBM price has surged $150–153/mt higher over the past week.

LNG’s premiums over LBM in Rotterdam have narrowed for a third consecutive week, falling by $39/mt to $351–356/mt, depending on engine type.

The Gulf war has also lifted the front-month NYMEX Japan/Korea Marker (JKM), which has helped to push Singapore's LNG bunker prices up by $233–234/mt in the past week, also depending on engine type.

By Konica Bhatt

Please get in touch with comments or additional info to news@engine.online