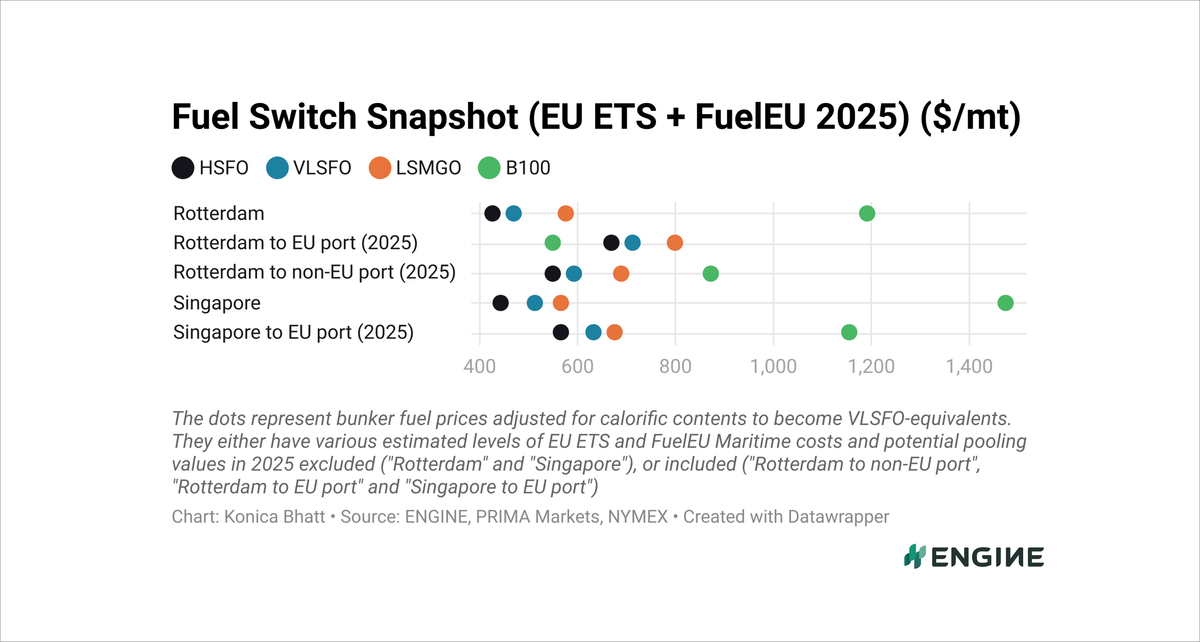

Fuel Switch Snapshot: B100 vs VLSFO divergence deepens

Rotterdam’s B100 more cost-effective against VLSFO

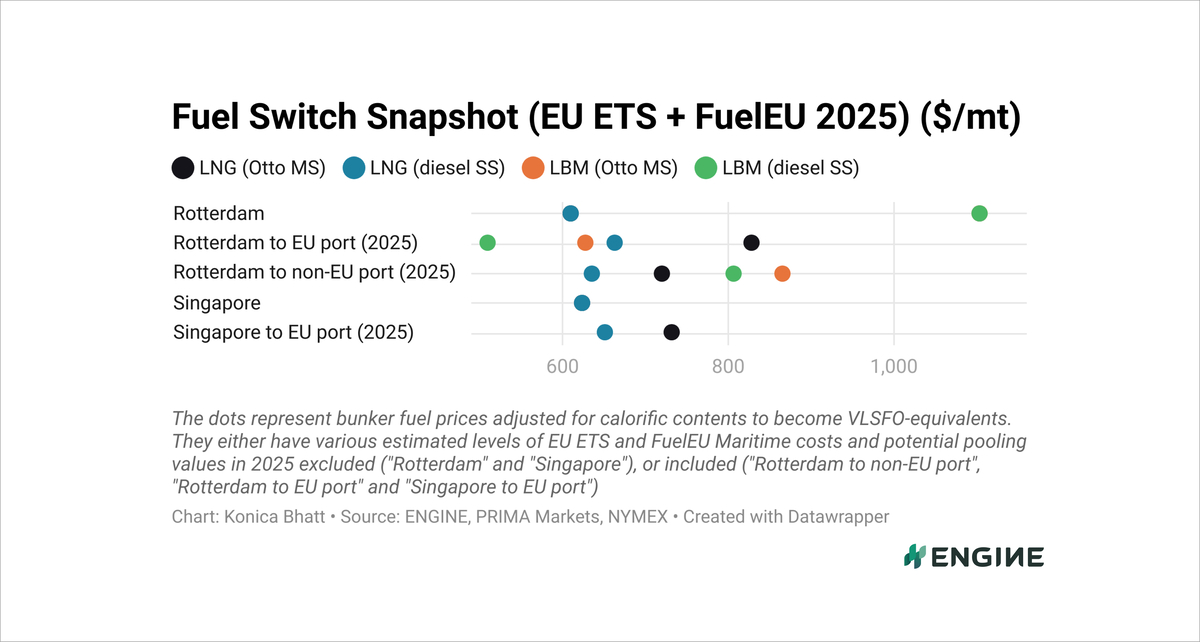

LBM nears $200/mt discount to LNG in Rotterdam

Rotterdam’s LNG bunker premium gains $5/mt

All bunker prices mentioned below have been adjusted for calorific contents to make them VLSFO-equivalent. They have estimated EU-EU voyage compliance costs included for Rotterdam, and non-EU-EU compliance costs included for Singapore. These account for EU ETS costs and FuelEU Maritime penalties, and our estimated compliance surplus values for FuelEU pooling. Rotterdam's B100 and LBM prices also factor in Dutch HBE rebates for advanced liquid and gaseous biofuels sold in the Netherlands.

B100’s discount to VLSFO in Rotterdam has widened by another $10/mt over the past week, to reach $162/mt for consumption between two EU ports.

B100 also remains the cheapest alternative for scrubber-fitted vessels bunkering in Rotterdam, now priced at a $119/mt discount to HSFO.

LNG now carries $152–199/mt premiums over liquefied biomethane (LBM) in Rotterdam, up $3-5/mt in the past week.

The LNG-LBM price range reflects the estimated cost of bunkering LNG and LBM for two types of LNG-capable engines, with EU compliance costs factored in. The lower end corresponds to vessels equipped with diesel slow-speed (diesel SS) engines with lowest methane slip, while the higher end applies to Otto medium-speed (Otto MS) engines, which have the highest methane slip.

For dual-fuel vessels, LNG is at a $115/mt premium over VLSFO when used in Otto MS engines. However, it shifts to a $50/mt discount to VLSFO when used in diesel SS engines with lower methane slips.

Liquid fuels

Rotterdam's VLSFO benchmark has increased by $10/mt over the past week, marking a third consecutive week of gains. The benchmark has risen by $53/mt since 12 May.

The recent price increase has partly been driven by persistent tight availability of the grade for prompt deliveries in the wider ARA region, where lead times are now recommended at around 7–8 days. A modest uptick in front-month ICE Brent futures has also added some upward pressure.

Rotterdam’s B100 benchmark has remained largely stable, with a slight $1/mt decline.

Singapore’s VLSFO price has declined by $10/mt over the same period. Lead times for the grade have increased from 6–13 days to 9–14 days.

Liquid gases

Rotterdam’s LNG bunker price has risen by $18–19/mt, linked to a 2% increase in the front-month Dutch TTF Natural Gas contract. The contract has been pushed higher by a bullish overall market sentiment and concerns over potential supply disruptions from Norway.

An uptick in Rotterdam's LNG bunker premium has also contributed to the port's LNG bunker price gain. The premium has gone up by about $5/mt over the past week to reach $135/mt.

In Singapore, the LNG bunker price has increased by $27–28/mt, supported by a 5% rise in the front-month NYMEX Japan/Korea Marker (JKM) gas contract. The increase has largely been driven by stalled Russia-Ukraine peace talks and a growing market focus on summer demand trends.

Major Asian countries like Japan and South Korea usually import more LNG for power generation when air condition demand increases in the summer. Temperatures typically get higher between June and September.

By Konica Bhatt

Please get in touch with comments or additional info to news@engine.online