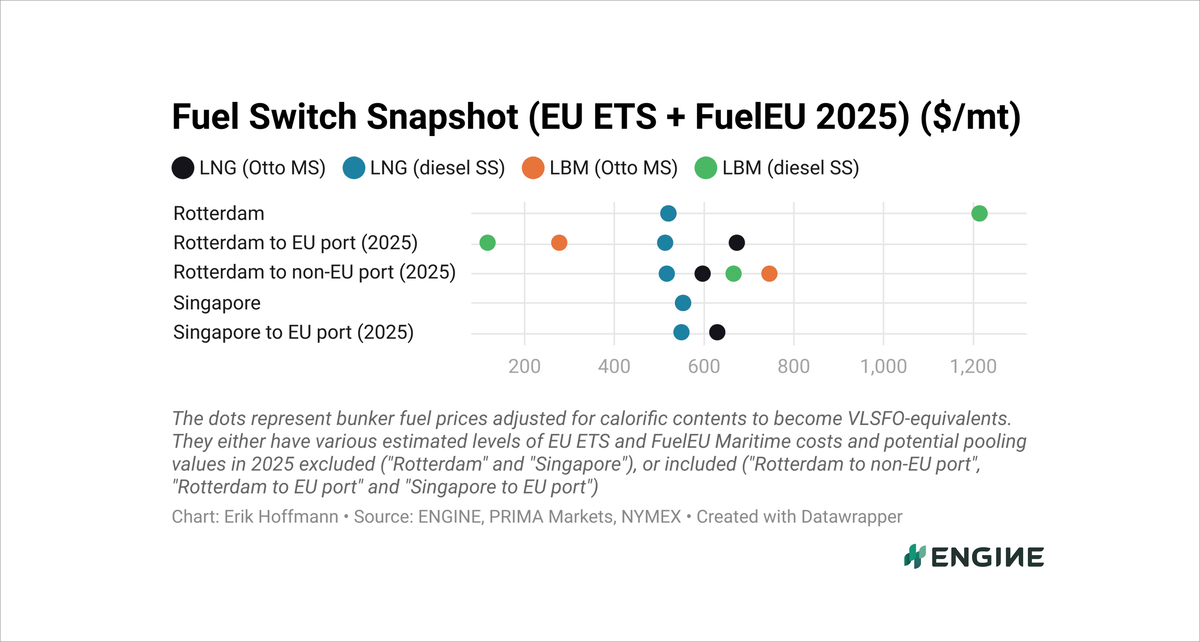

Fuel Switch Snapshot: EU rules push LBM around $400/mt below LNG

Prices drop across the board at major ports

LBM EU-EU compliance edge grows further

Singapore’s B100 still $400/mt above VLSFO

All bunker prices described in the text below have been adjusted for calorific contents to make them VLSFO-equivalent. They have estimated EU-EU voyage compliance costs included for Rotterdam, and nonEU-EU compliance costs included for Singapore. These account for EU ETS costs and FuelEU Maritime penalties, and the average price of compliance surpluses we have picked up from the FuelEU pooling market from the past week. Rotterdam's B100 and LBM prices also factor in Dutch HBE rebates for advanced liquid and gaseous biofuels sold in the Netherlands.

Rotterdam’s HBE-rebated liquefied biomethane (LBM) remains the cheapest compliance option for EU-EU voyages, despite dramatic price cuts across the board.

ENGINE’s assessed pooling estimates for LBM sold at 0 gCO2e/MJ have strengthened by $8–9/mt, with the average across seven surplus prices collected this week holding steady at roughly €216/mtCO₂e.

This means a dual-fuel ship sailing between EU ports and selling the compliance surplus it generates from using LBM instead of VLSFO now has a theoretical FuelEU pooling benefit of $938/mt for vessels with Otto MS engines and $1,099/mt for vessels with diesel SS engines.

LBM is treated as zero-carbon under the EU ETS. Combined with the theoretical pooling value and the Dutch HBE rebate, this can reduce the effective cost of bunkering LBM in Rotterdam to $116–277/mt.

For comparison, LBM is at a $202–363/mt discount to B100, a $396/mt discount to fossil LNG and a $371–532/mt discount to VLSFO in Rotterdam, depending on the vessel’s engine type and methane slip profile.

Liquid fuels

Rotterdam’s conventional fuel benchmarks have dropped sharply by $59-66/mt over the past week. The port’s HBE-rebated B100 has also fallen by $55/mt, a move amplified by a $7/mt rise in Dutch HBE rebates for marine B100.

These declines have widened B100’s discounts to HSFO and VLSFO by $21–25/mt on the week. On the other hand, its discount to LSMGO has narrowed slightly by $10/mt, to $398/mt.

The ENGINE-assessed FuelEU Maritime pooling value for B100 consumed on EU–EU voyages has risen by $6/mt to $676/mt.

Singapore’s conventional fuel prices have also declined, though more modestly, by $25–38/mt in the past week.

Its B100 price has dropped by $27/mt. Even then, B100 remains $227–549/mt more expensive than Singapore’s conventional grades, with its VLSFO spread widening by $1/mt to $467/mt.

The potential pooling value for B100 on nonEU–EU voyages from Singapore has risen by $3/mt on the week to $338/mt.

Liquid gases

Rotterdam’s LNG price has plunged by a steep $69–70/mt over the past week, while its LBM benchmark has also fallen sharply by $42/mt.

LNG’s drop is mainly tied to a 7% slide in the front-month Dutch TTF natural gas contract, which has eased on steady Norwegian supplies and expectations of higher temperatures across northwestern Europe.

Singapore’s LNG bunker price has slipped by a more modest $16/mt on the week. The price has tracked the downturn in the NYMEX Japan/Korea Marker, which has been weighed down by high stockpiles and sluggish gas demand in Northeast Asia.

By Konica Bhatt

Please get in touch with comments or additional info to news@engine.online