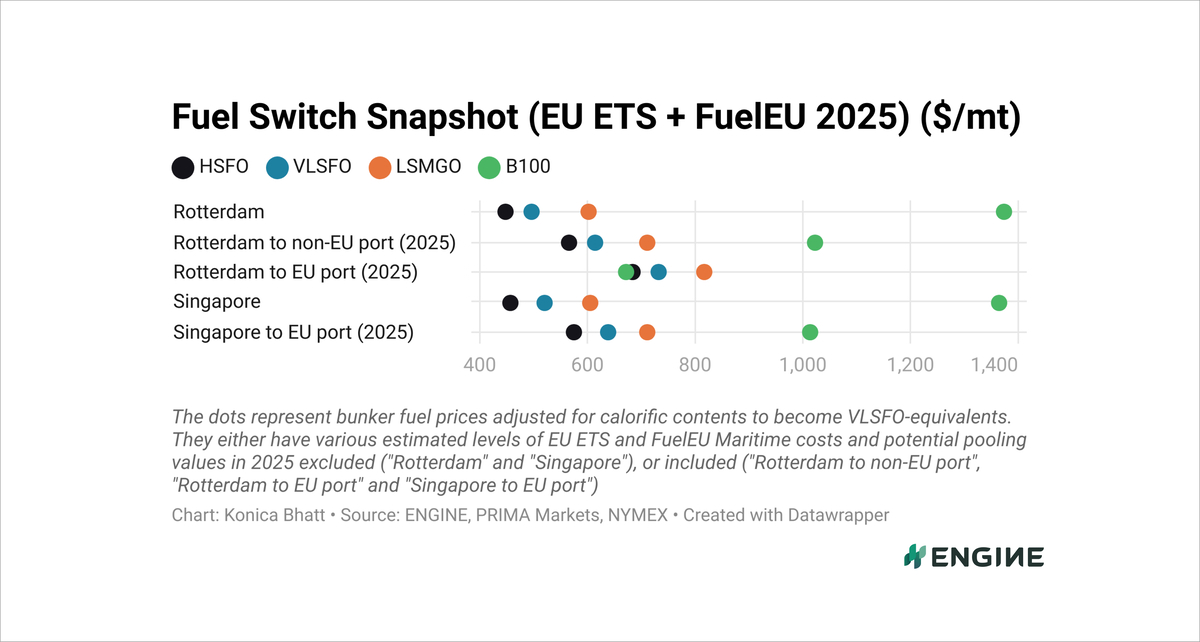

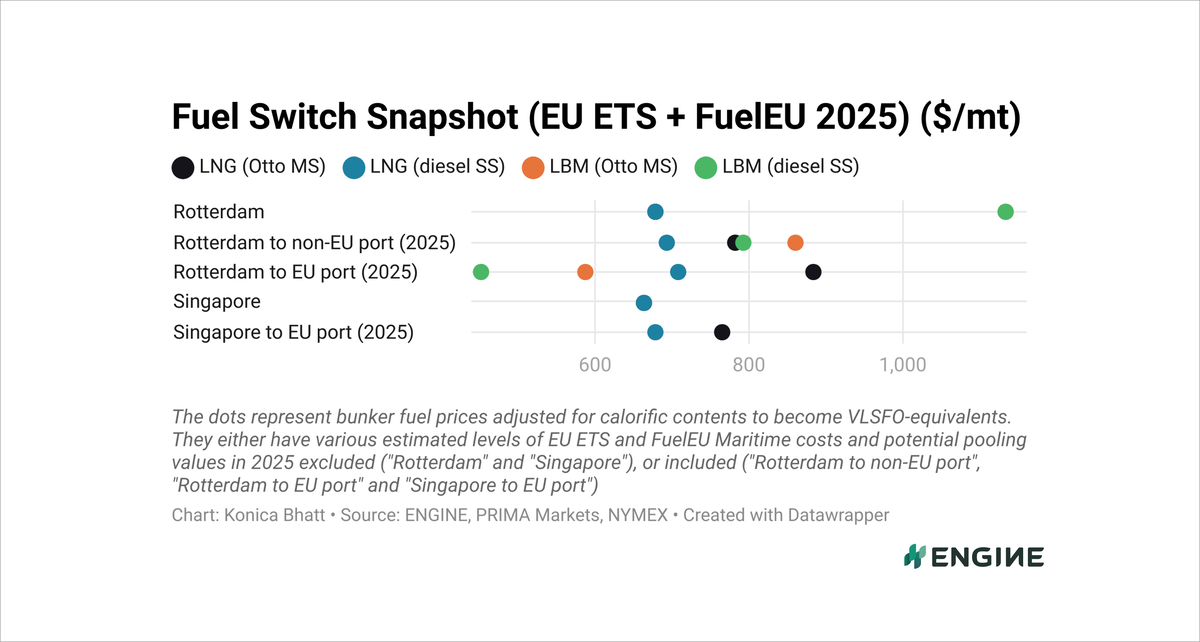

Fuel Switch Snapshot: Huge potential pooling values for B100 and LBM

B100 discounts to conventional fuels widen

Low-slip LBM at $256–279/mt discounts to LNG and VLSFO

All bunker prices mentioned below have been adjusted for calorific contents to make them VLSFO-equivalent. They have estimated EU compliance costs for EU–EU voyages included. These account for EU ETS costs and FuelEU Maritime penalties, and our estimated compliance surplus values for FuelEU pooling. Rotterdam's B100 and LBM prices also factor in Dutch HBE rebates for advanced liquid and gaseous biofuels sold in the Netherlands.

Rotterdam's B100 (100% biofuel) overall cost discount to HSFO has widened from $3/mt to $13/mt over the past week. And B100 is at an even larger discount of $59/mt compared to VLSFO in Rotterdam.

EU regulations make B100 considerably more attractive for EU-EU voyages, while HSFO and VLSFO will take hits from both FuelEU penalties and EU ETS carbon costs.

We assume that the FuelEU pooling value of B100 is equal to the price premium of the cheapest compliance option to be just compliant (roughly 3% biofuel with heavy fuel oils) over HSFO and VLSFO, multiplied by the number of vessels B100 can cover with its compliance surplus.

This is a conservative estimate of a pooling value that is not fixed, but rather determined in opaque over-the-counter markets that can involve shipping companies, fuel suppliers and other market makers.

We have also seen approaches where pooling values have been determined with bid-ask spreads, fossil and biofuel price indexing, and as a percentage discount to the default FuelEU penalties. The price undercompliant shipping companies will pay for overcompliant vessels' compliance surpluses will also typically include admin costs and a margin for the market makers.

If we had assumed a greater pooling value, that would have made B100 and LBM look even better against the fossil fuels in our Fuel Switch Snapshot.

LBM sold in Rotterdam and burned in a diesel slow speed engine remains the cheapest compliance option. This is the engine type with the lowest default methane slip factor in the FuelEU regulation. LBM also comes in at a $256/mt lower cost than LNG consumed in the same engine type, and $279/mt lower than VLSFO.

Liquid fuels

Rotterdam’s VLSFO benchmark has remained largely steady, with a modest $5/mt rise in the past week. The grade’s availability remains tight for very prompt delivery dates, with recommended lead times of 5-7 days.

The port’s B100 price has seen a smaller $2/mt rise in the past week. PRIMA Markets has assessed the Dutch HBE rebate to $353/mt now, down $3/mt over the week.

Singapore’s VLSFO benchmark has increased by $14/mt in the past week. Lead times now range from 2–10 days in the port, shortening from 3–12 days in the week prior.

Liquid gases

Rotterdam’s LNG bunker price has remained unchanged amid a broadly stable front-month Dutch TTF Natural Gas contract.

“On the gas market, fluctuations were rather modest… A lot of focus still centers around the Russian-Ukrainian wars,” Energi Danmark noted.

Singapore’s LNG bunker price has fallen for a fifth consecutive week. The benchmark has moved $7/mt lower in the past week, driven largely by market expectations of easing geopolitical tensions.

By Konica Bhatt

Please get in touch with comments or additional info to news@engine.online