Fuel Switch Snapshot: LNG bunker premiums narrow

Price drop reduces LNG’s gap with conventional fuels

LNG stays the second-priciest alternative in major ports

B24-VLSFO discount to B24-LSMGO widens in Singapore

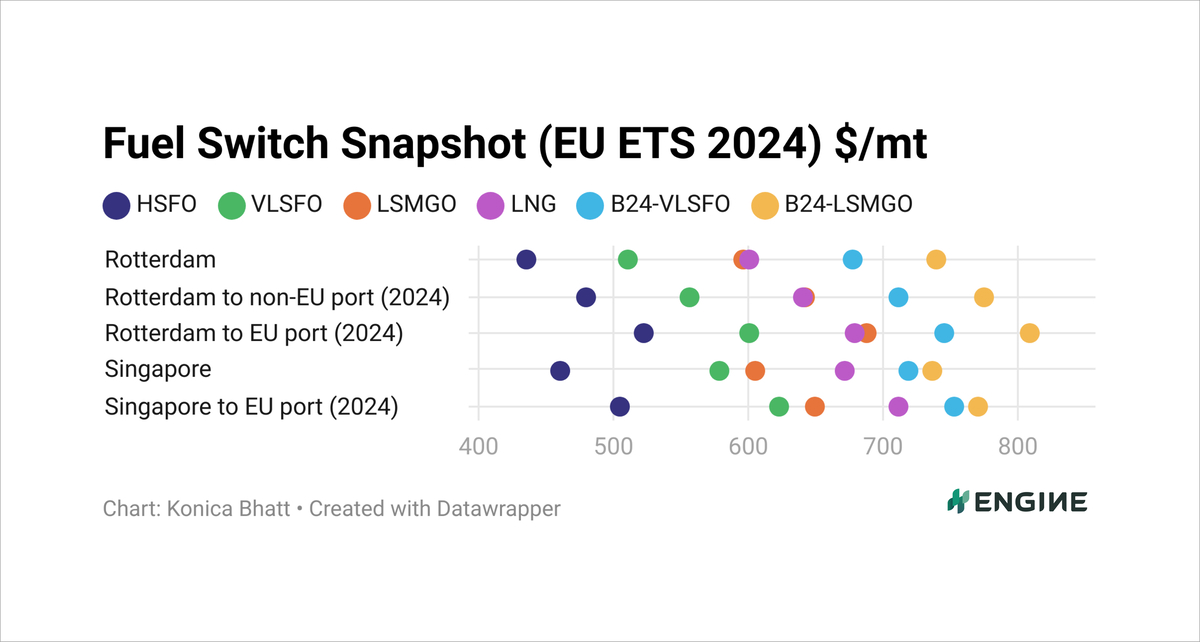

CHART: The dots represent bunker fuel prices adjusted for calorific contents to become VLSFO-equivalents, and with various estimated levels of EU ETS costs in 2024 excluded (Rotterdam) and included (Rotterdam to non-EU port and Rotterdam to EU port). ENGINE, PRIMA Markets, NYMEX

CHART: The dots represent bunker fuel prices adjusted for calorific contents to become VLSFO-equivalents, and with various estimated levels of EU ETS costs in 2024 excluded (Rotterdam) and included (Rotterdam to non-EU port and Rotterdam to EU port). ENGINE, PRIMA Markets, NYMEX

Sharp drops in Singapore and Rotterdam’s LNG bunker prices have narrowed their price premiums over conventional fuels in the past week.

Rotterdam LNG's premium over its VLSFO has decreased by $30/mt to $90/mt and its premium over its LSMGO has dropped by $27/mt to just $5/mt. If we factor in the estimated EU Allowances (EUAs), LNG is $2-8/mt cheaper than LSMGO in the port.

Meanwhile, Singapore LNG's premium over VLSFO has declined by $23/mt to $94/mt, and its premium over LSMGO has dropped by $36/mt to $67/mt.

B24-VLSFO in Singapore has shifted further from B24-LSMGO, with its discount increasing from $9/mt to $18/mt in the past week.

VLSFO

Rotterdam's VLSFO price has remained steady over the past week, with just a $6/mt increase, contrasting the significant $2.88/bbl ($21/mt) rise in the front-month ICE Brent futures contract.

Availability of the grade remains good in the port and most suppliers are able to offer prompt deliveries, a trader said. In addition, demand for the grade remains low, the trader added. Ample availability coupled with low demand appear to have capped any significant price gains for VLSFO.

Singapore’s VLSFO price has dropped by $7/mt in the past week, shunning Brent’s rise. Availability in the port remains tight, with lead times now extending up to 15 days, compared to 11 days the week prior.

ENGINE recorded 15 VLSFO stems in Singapore during the past week. Of these, 14 lower-priced stems were fixed for non-prompt deliveries – with lead times of more than seven days – priced between $564-579/mt. Only one stem was fixed for prompt delivery, priced around $30/mt higher than the non-prompt stems. The lower-priced stems appear to have contributed to the benchmark's decline.

Biofuels

Singapore's B24-VLSFO UCOME price has decreased by $5/mt, while its B24-LSMGO UCOME price has risen by $4/mt in the past week.

Suppliers in Singapore sold about 68,000 mt of bio-blended bunkers in August, up from 49,000 mt sold in July. Bio-blended bunker sales grew for the second consecutive month in August and were the highest since October 2023, according to preliminary figures from the port authority. Despite a jump in sales in August, spot demand for bio-bunkers in Singapore remains low, two sources said.

Rotterdam’s B24-VLSFO HBE and B24-LSMGO HBE prices have gained by $8-9/mt in the past week. These increases are supported by a $6/mt rise in the underlying ENGINE conventional VLSFO price and a $4/mt rise in conventional LSMGO price.

Additionally, a $19/mt increase in the underlying PRIMA's POMEME CIF ARA price has added further upward pressure on both biofuel benchmarks.

LNG

Rotterdam's VLSFO-equivalent LNG bunker price has plunged by $24/mt over the past week. The fall reflects a decline in the front-month NYMEX Dutch TTF Natural Gas contract, driven by Europe’s high gas storage levels, which continue to weigh on prices and signal ample supply in the market.

Singapore’s VLSFO-equivalent LNG bunker price has also plummeted $30/mt in the past week, partly due to the NYMEX Japan/Korea Marker (JKM) contract rolling over from the higher-priced October contract to the lower-priced November contract.

Softening demand for LNG cargoes in Asian markets has further pressured the JKM benchmark.

By Konica Bhatt

Please get in touch with comments or additional info to news@engine.online