Fuel Switch Snapshot: LNG premium over VLSFO widens

Higher European gas demand boosts price

Rotterdam LNG costs $200/mt more than VLSFO

B100 compliance premium over VLSFO drops

A sharp rise in Rotterdam's LNG's price has widened its premium over VLSFO by $67/mt in the past week. VLSFO-equivalent LNG is now $205/mt more expensive than VLSFO in Rotterdam when used in Otto medium-speed engines with a 3.1% methane slip.

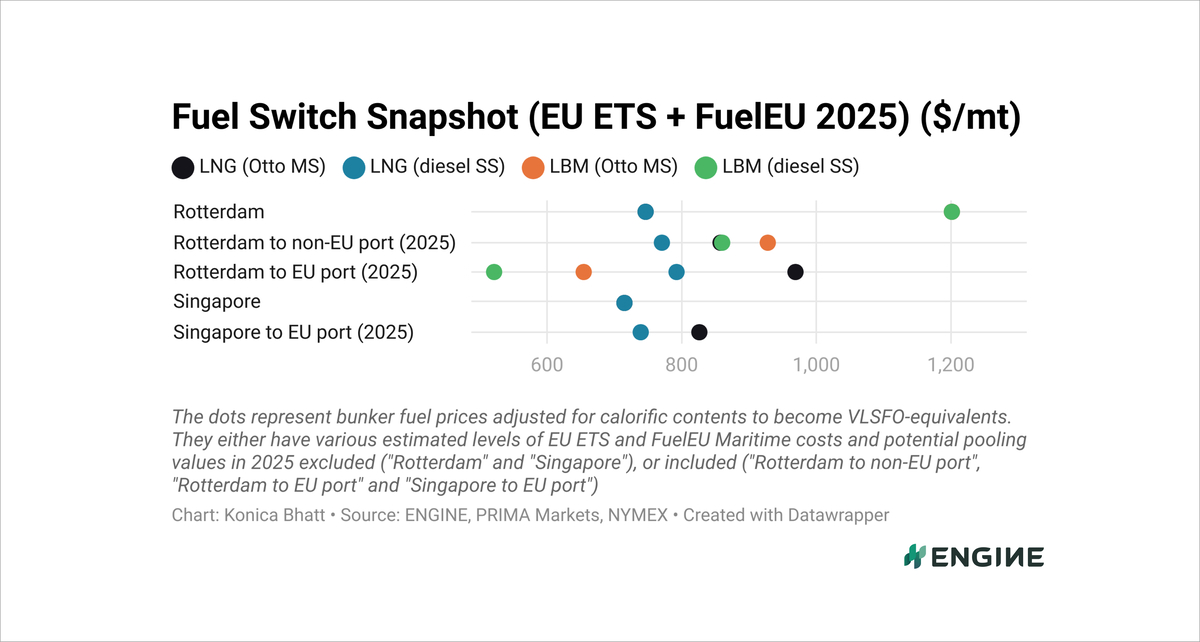

Even after factoring in EU-EU port compliance costs and estimated FuelEU Maritime pooling benefits, LNG remains $173/mt costlier than VLSFO.

When compliance costs and estimated pooling benefits are included, B100 has been at a $55/mt discount to HSFO and a $126/mt discount to VLSFO over the past week. This is a significant increase from the $11/mt and $83/mt discounts seen in the previous week.

Similarly, compliance costs and pooling benefits have increased LBM’s discount to fossil LNG by $6–9/mt, depending on the engine type, bringing it to $273–313/mt. The cost advantage also includes the Dutch HBE rebate for sustainable biogases.

Liquid fuels

Rotterdam's VLSFO-equivalent B100 price has fallen by a sharp $60/mt in the past week, reducing its compliance premium over VLSFO by $47/mt to $575/mt.

PRIMA assessed the Dutch HBE rebate for B100 at $364/mt, up $16/mt from the week prior.

Using B100 instead of VLSFO on ships offers a theoretical pooling benefit of $553/mt under FuelEU, reflecting a $21/mt decrease from the previous week. B100 is considered zero-carbon in the EU ETS which, combined with the theoretical pooling benefit, can reduce the real cost of bunkering B100 to $670/mt.

Rotterdam’s VLSFO price has dropped by a modest $8/mt over the past week, compared to a bigger $17/mt decline in front-month ICE Brent Futures. Fuel availability remains stable across the wider ARA region, with suppliers generally recommending lead times of 3–5 days.

VLSFO availability remains tight in Singapore. The benchmark has fallen by $20/mt in the past week, mostly in tandem with Brent's decline.

Liquid gases

Rotterdam’s VLSFO-equivalent LNG price has surged by $59/mt in the past week, partially driven by a 3% rise in the front-month Dutch TTF Natural Gas contract. Increased gas demand, spurred by colder-than-usual temperatures in Europe, has boosted the TTF benchmark, Rystad Energy noted.

Meanwhile, Singapore’s VLSFO-equivalent LNG price has increased by a smaller $18/mt over the past week. This slight increase can partly be attributed to a modest rise in the front-month JKM contract, driven by tepid LNG demand across Asia due to warmer-than-usual weather.

While the VLSFO-equivalent price of liquefied biomethane (LBM) is over $400/mt higher than fossil LNG in Rotterdam, the gap narrows significantly when accounting for EU-EU compliance costs and pooling benefits.

LBM consumed in Otto MS engines with a 3.1% methane slip generates a theoretical pooling benefit of $546/mt under the FuelEU mechanism. When used in diesel SS engines with a 0.2% methane slip, LBM offers a significantly higher pooling benefit of $681/mt. These pooling benefits have remained unchanged over the past week.

When including compliance costs and pooling, the cost of bunkering LBM can be reduced to $520-655/mt, while the price of fossil LNG increases to $793-968/mt – depending on the engine type.

By Konica Bhatt

Please get in touch with comments or additional info to news@engine.online