Q&A: Green corridors key to a systemic green shipping transition – Mærsk Mc-Kinney Møller Center for Zero Carbon Shipping

Green corridors can pave the way for whole value chains for zero-carbon marine fuels and accelerate first-mover initiatives. The Mærsk Mc-Kinney Møller Center for Zero Carbon Shipping has therefore devoted its time and resources to push for several green corridors, its head of energy and fuels, Torben Nørgaard told ENGINE in a recent interview.

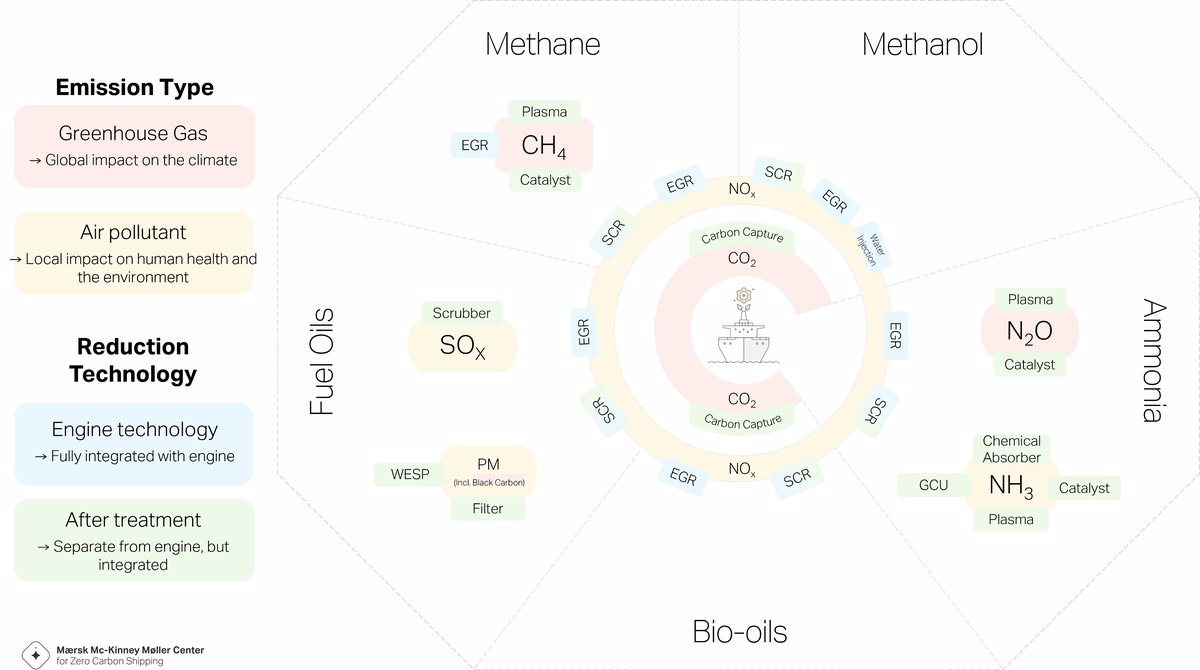

PHOTO: The Center launched an Emissions Web in July which shows emission risks for fuel oil and four alternative fuel types, along with technologies that can be applied to curb emissions. Mærsk Mc-Kinney Møller Center for Zero Carbon Shipping

PHOTO: The Center launched an Emissions Web in July which shows emission risks for fuel oil and four alternative fuel types, along with technologies that can be applied to curb emissions. Mærsk Mc-Kinney Møller Center for Zero Carbon Shipping

What are the bottlenecks to developing large, ocean-going zero-carbon and zero-carbon ready ships?

The economic gap between current operation and low emission operation remains too high to unlock the significant investments required. Along the entire value chain from production through infrastructure, ports, and vessel we see first mover initiatives. To promote the transition at a more systemic level the drive towards establishing green corridors is a main driver to integrate the entire value chain and at the same time linking to government and regulatory support and private - public partnership. We at the Center have chosen to invest our resources in several green corridor initiatives to enable and accelerate first mover initiatives.

If we think about the supply chains for alternative fuels with zero-carbon potential like green hydrogen, green ammonia, methanol, and biofuel (B100), would it be fair to say that there are equally big challenges to be overcome across production and sourcing, storage and bunker supply, ship engine technology, and safe handling and storage onboard ships?

It is fair to say that every scalable low emission fuel may have a role to play while implementing the energy transitions. For deep sea shipping we have identified ammonia, methanol, methane, and bio-oils as potential future energy carriers for the maritime industry. Each of these energy carriers have unique challenges within safety, life cycle assessment, production efficiency, and capture of economies of scale that must be addressed for the energy carrier to contribute to the energy transition at scale.

The coming decades are believed to hold room for multiple zero-carbon fuel alternatives. But do you see a front-runner for this decade – a fuel type that is likely to kickstart the energy transition for large, ocean-going ships?

It is correct that none of the low emission fuel are likely to scale in time to fulfil the fuel demand of the industry. Hence, from a fuel perspective we cannot point at a single winner. Rather, we are looking into a transition where flexibility in design and operation will carry value. Already today bio-oils and bio-methane may be supplied used to partially substitute fuel oil and LNG. Methanol has high technical readiness level but lacks supply and has challenges related to scalability. Ammonia has better scalability - initially and potentially produced via natural gas combined with carbon capture storage and subsequently produced via electricity and electrolysis of water – but lacks readiness on onboard propulsion technology and safe bunker and vessel design and operation.

Is the availability and price of promising future fuels ultimately going to determine their wider uptake in the industry? Or are there other sticking points?

Scalability and cost of production will be two of the leading parameters for the future fuels. Competition for the energy from other sectors will support scalability but also influence pricing of the fuels thereby establishing a margin between cost and price of the fuels. Another key point is the establishment of a life cycle assessment methodology that allows us to distinguish between fuels in accordance with emissions and environmental impact along the full production chain – i.e., on a well-to-wake basis. This to ensure that development, policies, regulation, and investment are targeted towards the high impact transition pathways.

Connecting continents without emissions

In March, the Mærsk Mc-Kinney Møller Center for Zero Carbon Shipping (the Center) announced a green corridors network spanning Hamburg, Gdynia, Ronne, Rotterdam and Tallinn. Dubbed the European Green Corridors Network, these corridors are meant to demonstrate that zero-carbon shipping can be done commercially and may provide a blueprint for how to scale supply chains for alternative fuels.

The Center followed up with another green corridor announcement in April, after it had struck a deal with Chile’s Ministry of Energy. Chile has been brought forward as a country with great potential for zero-carbon fuels production as it can tap into its abundant sources of renewable energy, especially solar and wind power generated in its Magallanes and Antofagasta regions.

Green shipping is pivotal to Chile’s own decarbonisation plan, as it is heavily dependent on domestic and international maritime transport. By the end of the year, the Center and Chile aim to have mapped out the most suitable green corridors for the project, based on emission intensity, fuel availability, distance to ports, vessel segments and routes.

Another big green corridor announcement came last month. The port authorities of Singapore and Rotterdam – the world’s top two for bunkering – unveiled plans to develop what could become the world’s longest green corridor. They aim for vessels powered by low- and zero-carbon fuels to sail on this key shipping route by 2027.

The Center is one on the partners on the Singapore-Rotterdam corridor project, along with the Singapore-based Global Centre for Maritime Decarbonisation and some of the world’s biggest energy and shipping companies including Shell and CMA CGM.

In a different initiative, Singapore's port authority has teamed up with a range of players to explore the port's potential for building ammonia infrastructure to cater to future shipping demand.

Rotterdam, for its part, oversaw the world’s first barge-to-ship methanol bunkering operation at its Vopak Terminal Botlek last year. This year it announced a hydrogen import target of 4.6 million mt/year by 2030, and that ammonia producer OCI will expand its ammonia import terminal to triple throughput capacity by 2023 and create a hub for ammonia bunkering.

By Erik Hoffmann

Please get in touch with comments or additional info to news@engine.online