The Week in Alt Fuels: LBM rules the pool

Liquefied biomethane (LBM) stands out as a compliance fuel for shipowners looking to get bang for their buck in the EU, with some already bunkering more of it instead of LNG.

IMAGE: A Gasum bunker vessel supplying LBM to a Hapag-Lloyd containership in Wilhelmshaven. Linkedin of Gasum

IMAGE: A Gasum bunker vessel supplying LBM to a Hapag-Lloyd containership in Wilhelmshaven. Linkedin of Gasum

FuelEU Maritime requires ships to meet a greenhouse gas (GHG) intensity limit for EU-linked voyages. Their GHG intensity is measured in grams of CO2-equivalent per megajoule (gCO2e/MJ).

When ships outperform these limits, they generate a compliance surplus that can be transferred or sold in a pool of ships. This market mechanism is quietly shifting LBM from a niche compliance option to one of the most commercially attractive fuels in the European market.

FuelEU green compliance ace

ENGINE calculations using default FuelEU emission factors show that the fuel’s well-to-wake GHG intensity can range from 16 gCO2e/MJ for vessels with diesel slow-speed engines (0.2% methane slip) to 30 gCO2e/MJ for vessels with Otto medium-speed engines (3.1% methane slip).

Even at the upper end, LBM's default GHG intensity is around three times lower than FuelEU’s 2025 cap of 89.34 gCO2e/MJ.

This makes it a prime candidate for pooling. One LBM-powered vessel can theoretically balance out compliance deficits of 32-40 heavy fuel oil (HFO)-powered vessels or 36-45 LNG ones. It will remain hugely overcompliant even as the cap tightens to 62.90 gCO2e/MJ in 2040, though the number of offset vessels would shrink.

Low carbon, high value

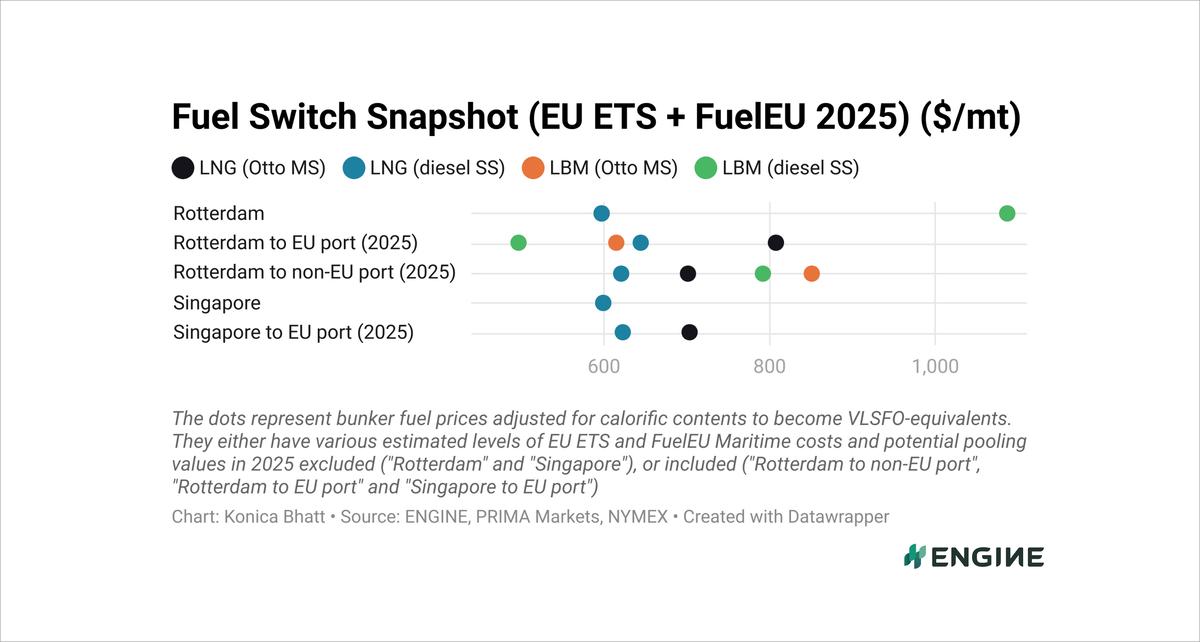

The economics reinforce its appeal. We estimate that LBM sold with Dutch HBE-rebates in Rotterdam can have pooling values of between $470-590/mt for voyages between two EU ports, depending on an engine's methane slip.

This is assuming that the compliance surplus generated from using LBM on a vessel can be sold in a FuelEU pool. And that this value is equivalent to the extra cost of buying just enough LBM to make an LNG-fuelled vessel with an Otto medium-speed engine (91.03 gCO2e/MJ) compliant with today's 89.34 gCO2e/MJ GHG intensity target.

LBM is also an attractive way of avoiding EU Emissions Trading System (EU ETS) costs as it has a carbon factor of zero.

This all means that LBM bunker prices in Rotterdam can potentially drop to around $500-610/mt. For dual-fuel LNG vessels, that makes LBM the lowest-cost route to compliance.

Scaling with surplus

Several shipowners have already moved to capitalise on these favourable LBM economics. Finnish ferry operator Wasaline and Sweden’s Viking Line have partnered with Gasum to build a pooling model centered on LBM-powered routes.

Wasaline operates one LNG/LBM-capable ferry between Finland and Sweden, Viking Line another between Stockholm and Visby. Both are expected to run daily routes on LBM, generating overcompliance for the pool.

Gasum will manage the mechanism, supply the LBM and also operate one of its own chartered dual-fuel bunkering vessels, Kairos, on LBM to increase the surplus. It will then sell this surplus to shipowners operating fossil-fuelled ships that need to close their compliance gap.

The pooling mechanism “has the potential to increase the production and use of renewable biofuels” by creating a commercial path to scale, Wasaline’s chief executive Peter Ståhlberg said.

It will also help other shipowners to lower their emissions and “drive the green transition forward in our industry, he added.

Norwegian shipping company United European Car Carriers (UECC) is following a similar path. With 42% of its fuel mix comprising LBM, LNG and biofuels, UECC has already brought its fleet-wide intensity down to 68 gCO2e/MJ so far. That is a 25% reduction from its 2014 baseline and well below FuelEU's target. It operates five LNG/LBM-capable ships and has a supply agreement with Titan to secure future LBM volumes.

UECC intends to achieve GHG intensity of 57 gCO2e/MJ this year based on its current supply plan, then further reduce it to 41 gCO2e/MJ by 2030 by using 58% alternative fuels.

This strategy supports long-term compliance. “UECC will never be in a position of needing to borrow compliance from other vessels,” UECC's sustainability manager Daniel Gent told ENGINE in January.

Beyond the pool

And LBM’s momentum doesn’t seem to be limited to FuelEU pooling. Container liner Hapag-Lloyd recently bunkered two of its dual-fuel vessels with 4,800 mt of LBM in Rotterdam and Wilhelmshaven, supplied by Gasum.

Hapag-Lloyd took on LBM as part of a low-emission fuel tender issued by the Zero Emission Maritime Buyers Alliance (ZEMBA), a consortium of major cargo owners including Amazon and Nike. Hapag-Lloyd won the tender to reduce its emissions by 82,000 mtCO2e compared to running on conventional fuels between 2025-2026.

The shipping firm will allocate carbon credits to ZEMBA members through a book-and-claim system, based on the GHG reductions it achieves from its LBM-fuelled voyages between Europe and Asia. This system allows the cargo owners to claim voluntary Scope 3 emission savings by paying premiums for carbon credits to Hapag-Lloyd and other shipping companies.

In other news this week, OCI HyFuels has supplied 500 mt of bio-methanol to Dutch marine contractor Van Oord's dual-fuel offshore installation vessel in Amsterdam. This marked the first ship-to-ship bio-methanol bunker operation in the port.

German engine manufacturer MAN Energy Solutions (MAN ES) plans to deliver a two-stroke methanol engine next month. MAN ES claims the engine is the most powerful methanol engine to date, and it will be the first of 12 engines that will power a series of 24,000 TEU-capacity container vessels currently under construction.

Commodity trading firm Trafigura has ordered four medium-sized ammonia-capable liquefied gas carriers from South Korea’s HD Hyundai Mipo shipyard. The dual-fuel vessels will be able to operate on ammonia or conventional fuels upon delivery in 2028.

By Konica Bhatt

Please get in touch with comments or additional info to news@engine.online