The Week in Alt Fuels: There will be margins

FuelEU Maritime's compliance market is finally starting to show its hand. Surplus prices are moving further from biofuel costs towards penalty levels, while some pool makers quietly test how much margin the market will bear.

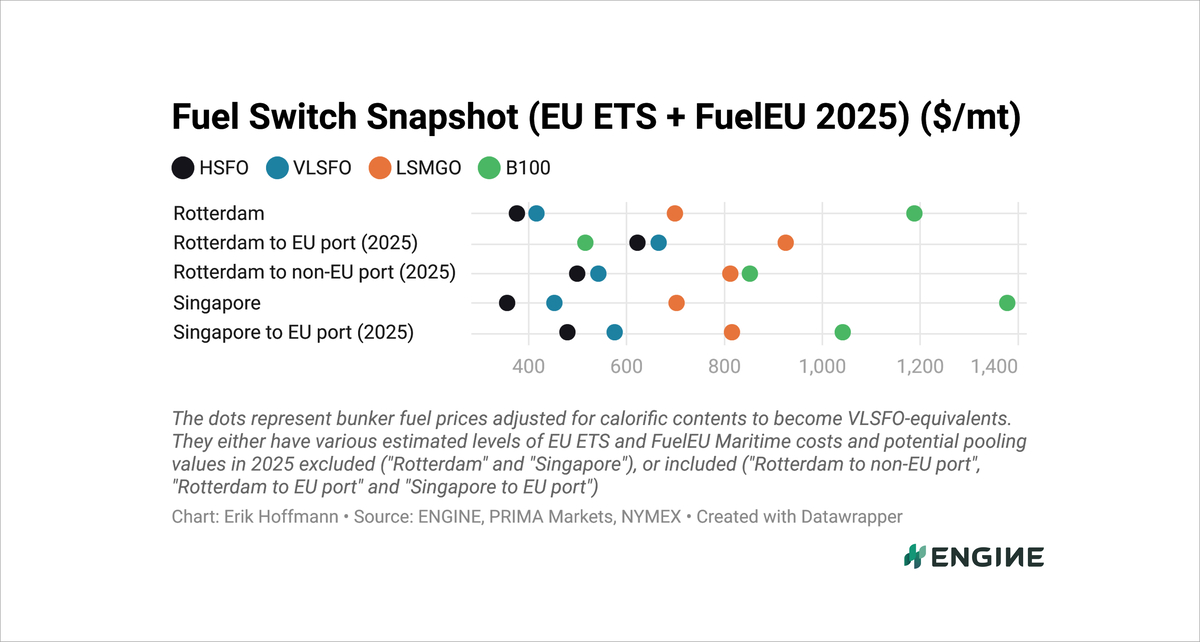

CHART: ENGINE's Fuel Switch Snapshot now take real, assessed FuelEU compliance surplus benchmarks into the equation

CHART: ENGINE's Fuel Switch Snapshot now take real, assessed FuelEU compliance surplus benchmarks into the equation

There is now more clarity on what levels FuelEU Maritime compliance surpluses are going for. These compliance markets are still fragmented and opaque, but market information we have gathered suggests that prices have been rising with demand and that trading margins could be lucrative.

How we priced the puzzle

Going into FuelEU’s 2025 debut year, ENGINE looked at various methodologies for setting compliance surplus values. Before we had access to a steady flow of real compliance surplus prices trading in the market, we had to estimate what the pooling value was. The pooling value was one of the key puzzles the European Commission left for the market to solve.

A lot of people have asked us this year how we arrived at our estimate. We did this completely as a spreadsheet exercise, where we first assumed that the price of compliance surpluses would sit in a range between the cheapest compliance option at the lower end, and the non-compliance penalty at the higher end.

The cheapest compliance option for most companies has been just enough biofuel to be compliant on a vessel level, bunkered with HBE-rebates in the Netherlands. The price premium of just enough bio-HSFO/VLSFO over the price of pure HSFO/VLSFO has been around $25-26/mt lately, while that for bio-LSMGO over pure LSMGO has been around $9-10/mt.

To gauge the true cost of B100 against HSFO/VLSFO/LSMGO, we multiplied those premiums by the number of HSFO/VLSFO/LSMGO-powered vessels B100 can take from a negative compliance balance to a net-zero balance towards the 2% greenhouse gas (GHG) intensity reduction target for 2025-2029. We also did energy conversions to make all the fuels VLSFO-equivalents and added EU ETS costs for fossil fuels.

That was the basis for our Fuel Switch Snapshots, which allowed us to compare energy- and EU regulation-adjusted prices for fossil fuels and alternative fuels in a much more complex bunker market than just a short year ago.

This methodology might still work for shipping companies transferring compliance between vessels in their own fleets, but given the recent rise of compliance surplus prices seen in pooling markets, we have decided to update our methodology to reflect that. We now value the compliance surpluses generated by fatty acid methyl ester (FAME) B100, liquefied natural gas (LNG) and liquefied biomethane (LBM) based on the prices we hear shipping companies selling them for.

What trading levels translate to

When a shipowner sells compliance surpluses into a pool, the shipowner can be offered a price way below the pool maker’s sell price to undercompliant owners. We have seen multiple offers to sellers into a pool at around €190-200/mt of carbon dioxide-equivalent (€190-200/mtCO2e) in the past week.

When we adjust to a $/mtFAME level, the potential pooling value comes to $590-620/mt for FAME B100 consumed between two EU ports. That pooling value can then be knocked off the higher price of FAME B100 to make it competitive against conventional fuel oils and gasoils that look seemingly cheaper at face value.

For LBM sold with a GHG intensity of 0gCO2e/MJ, the $/mtLBM pooling value is considerably greater at $820-860/mt for Otto medium speed (Otto MS) engines, and $960-1,010/mt for diesel slow speed engines.

Several pool market makers have indicated much higher sell levels, however. In recent weeks, we have seen indicative compliance surplus levels of €225-240/mtCO2e at the high end. That translates to $700-750/mt for FAME B100, $970-1,040/mt for LBM with Otto MS engines and $1,140-1,220/mt for LBM with diesel SS engines.

Pool makers test the spread

Some pool makers are trying to attract compliance surpluses from overcompliant ships into their pools at values that are lower than the values that they can sell those compliance surpluses to undercompliant ships for.

The difference can give them a chunky margin. If a pool maker is able to purchase compliance surpluses at €200/mtCO2e and sell at €230/mtCO2e, for example, that would give the pool maker a trading margin of $93/mt for FAME B100, $130/mt for LBM Otto MS and $152/mt for LBM diesel SS.

Other pool makers say they don’t take trading margins for each transaction. They act more like brokers to match bids and asks, like OceanScore which has registered wide price spreads of €180-230/mtCO2e on its platform in October-November, coming up from €175-210/mtCO2e in August-September. Larger lots have been going for a lot less than smaller lots, the company said.

Demand stretches the spread

Demand for these surpluses has been rising as more shipowners have caught up with the FuelEU regulation and seek to get out of penalties without going through the trouble of bunkering biofuels on their ships. That seems to have lifted the higher end of the price range to €230/mtCO2e after a slower summer.

OceanScore has said that more transparency about where prices sit contributed to narrow the price spread it was seeing on its platform, from a higher of €65/mtCO2e in June, to €55/mtCO2e in July and €35/mtCO2e in August-September. The jump in the top end has brought that spread up again, to €50/mtCO2e in October-November, which suggests that it is demand-driven and goes wider despite more transparency.

Gasum started publishing compliance surplus prices this month.

“We at Gasum believe a more transparent and standardized FuelEU Maritime compliance market is needed to support shipping companies in making the right decisions,” Gasum’s vice president of maritime Jacob Granqvist said.

The price Gasum lists daily is its actual selling price for a minimum of 500 mtCO2e, and it has ticked up from €225/mtCO2e to €230/mtCO2e in recent days.

Another pool maker has told ENGINE that it sells compliance at roughly that €225-230/mtCO2e level and that it has nearly sold out now. Buyers are already looking to secure compliance surpluses for next year. And a trader indication as high as €240/mtCO2e was also seen in the market in the past week.

Towards penalty discount pricing

Scarsity economics will have greater and greater influence on compliance surplus prices as the year draws to a close. Shipping companies that have not yet bunkered biofuels, LNG, LBM or green methanol on their ships soon won’t have the option to comply with FuelEU physically. Unless they kick into gear and source low-emission fuels now, they will have to pay penalties of €62/mt ($71/mt) for HSFO and VLSFO, and €39/mt ($45/mt) for LSMGO consumed between EU ports. Or half of those amounts sailing into and out of the EU.

Compliance surplus prices still sit somewhere between biofuel compliance costs and penalties. They could move much closer to penalty levels, especially after the New Year countdown, when one pool maker told us that surpluses could go as high as a 10% discount to penalties.

By Erik Hoffmann

Please get in touch with comments or additional info to news@engine.online