LNG Bunker Snapshot: Cold weather lifts prices in Rotterdam and Singapore

LNG bunker prices have shot up in both Rotterdam and Singapore, driven higher by cold weather and geopolitical risks.

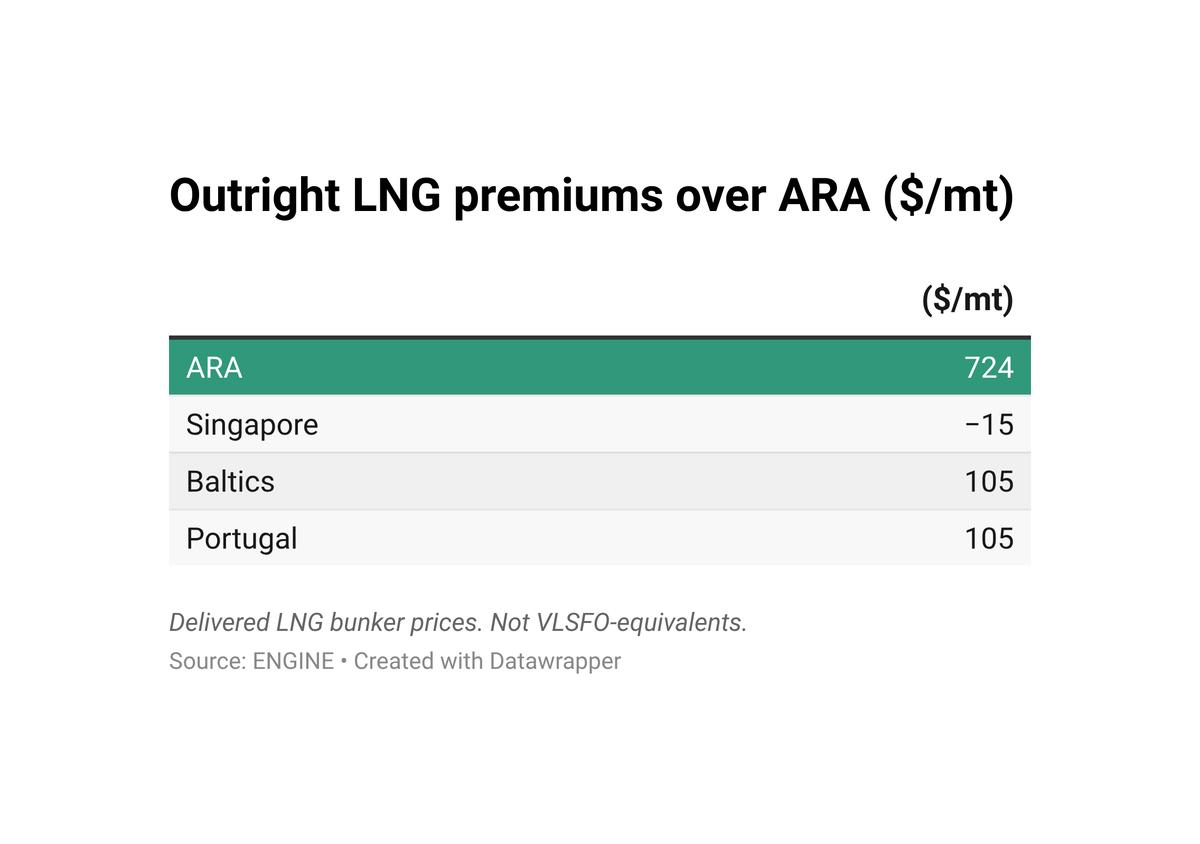

Weekly changes in LNG bunker prices:

- Rotterdam up by $81/mt to $724/mt

- Singapore up by $103/mt at $709/mt

Rotterdam

Rotterdam’s LNG bunker price has jumped, tracking a firmer front-month Dutch TTF natural gas contract, which climbed by $1.58/MMBtu over the week to $11.26/MMBtu ($586/mt).

The rise in TTF has been underpinned by a mix of fundamentals. Prices were supported by “colder weather, reduced wind power generation in Germany, and increased withdrawals from underground gas storage,” according to the Japan Organization for Metals and Energy Security (JOGMEC).

Forecasts for “colder-than-usual weather towards the end of January are proving bullish for prices,” two analysts at ING Bank said.

Colder conditions across Europe are sharpening competition for LNG. Europe is “set for another cold spell, which could drive stronger competition for flexible LNG cargoes,” said Greg Molnár, gas analyst at the International Energy Agency (IEA).

“Northwest Europe turned colder, lifting heating demand & gas-to-power burn,” commented Hendrian Sukardi, LNG market analyst at ENN Energy.

Prices “rallied… on the back of cold outlook and rapidly falling inventories,” Stephen Stapczynski, Energy Asia team leader at Bloomberg News, echoed.

Geopolitics have also played a role. Prices were further supported by “heightened geopolitical risks surrounding Iran,” JOGMEC said.

“In an increasingly fragmented world, fear on supply security naturally fuels more price volatility,” Molnár added.

Financial positioning has amplified the move. “Short-covering by investment funds” also contributed to pushing prices higher, JOGMEC said. Short-covering in the LNG market refers to funds buying back previously sold positions to close bets on falling prices, which can push prices upward.

“The net short positions of investment funds reached a near all-time high by the end of 2025. The rapid change in fundamental drivers means that there is now a surge to close out their open short positions and limit their losses... this amplifies further the price swing,” Molnár said.

On the supply side, nuclear outages added support.

“Flamanville nuclear plant (in France) is out until the end of Jan, supporting stronger gas burn in the power sector across northwest Europe,” Molnár said.

Storage levels underscore the tightening market. The EU’s underground gas storage stood at 50.9% on 16 January, down from 55.5% a week earlier and 19.1% lower year-on-year, according to Gas Infrastructure Europe.

Meanwhile, LNG bunker demand patterns shifted in December. December recorded the lowest monthly volume since May 2023, driven mainly by reduced container ship demand as several Hapag-Lloyd mega-boxships bunkered in Germany instead, Kpler said.

Shell pivoted accordingly: the 18,000 cbm Lotus delivered 29,000 cbm in the Netherlands in November but had no Dutch operations in December, instead focusing on Germany and Belgium. TotalEnergies’ 18,600 cbm Gas Agility also saw deliveries slip to 24,000 cbm from 31,000 cbm in November, the market intelligence firm added.

Singapore

Singapore’s LNG bunker prices have surged over the past week, climbing by $103/mt to $709/mt. The price, which stood at a $37/mt discount to Rotterdam a week earlier, has since narrowed to a $15/mt discount.

Singapore’s LNG bunker prices typically track the NYMEX Japan/Korea Marker (JKM). The JKM front-month contract rose by $1.59/MMBtu over the week to $11.16/MMBtu ($580/mt).

The rally has largely been driven by “increased spot trading activity by rising European gas prices” and “forecasts of colder temperatures in Northeast Asia,” according to Japan Organization for Metals and Energy Security.

North Asian prices also strengthened as weather risks mounted. LNG spot prices “rallied… as a forecast of cold weather threatens to drive up spot purchases by Japan and Korea. China would also see stronger demand, with temperatures across Beijing and Shanghai expected to plunge by 20°C this week,” said Daniel Hynes, senior commodity strategist at ANZ Bank.

Weather dynamics reinforced the outlook. “The cold snap is being driven by low-pressure systems high in the atmosphere, which are allowing the icy Arctic air to spill across several regions worldwide, including Asia. Temperatures in Beijing and Shanghai could plunge by about 20°C through Wednesday, as shown by forecasts from the China Meteorological Administration,” said Stephen Stapczynski of Bloomberg News.

Japan’s LNG inventories for power generation stood at 2.28 million mt as of 11 January, down by 10,000 mt from the previous week, based on data from the Ministry of Economy, Trade and Industry.

The price surge was further reinforced by a 19% rise in LNG bunker premiums, which moved from about $108/mt to $128/mt.

LNG bunker sales rose by 23% to 571,000 mt in 2025, with average daily volumes of around 1,600 mt, up from about 1,300 mt/day in 2024.

LNG bunker demand expanded sharply in 2025, with market research firm Kpler noting that LNG consumption for container ships climbed to 145 operations in 2025 from 98 in 2024, while demand from vehicle carriers rose to 168 operations from 61 in 2024.

All three LNG bunker vessels also recorded higher activity in 2025. Pavilion Gas’s 12,000 cbm Brassavola completed 114 calls, up from 92 in 2024. FueLNG’s 7,500 cbm Fuelng Bellina logged 134 calls, compared with 90 in 2024, while its 18,000 cbm Fuelng Venosa recorded 165 calls, up from 100 in 2024, Kpler added.

Other LNG bunker news

Singapore’s Maritime and Port Authority of Singapore (MPA) has invited applications for additional licences to supply LNG as a marine fuel at the port.

According to DNV, 193 LNG-capable vessels entered service in 2025, up from 177 LNG-capable deliveries in 2024. The global fleet now comprises 846 LNG-capable vessels in operation, with a further 642 vessels on order for delivery by 2033.

“LNG remained the biggest driver throughout the year, with 188 orders accounting for 68% of alternative-fuelled newbuilds and 31% of overall gross tonnage,” said Kristian Hammer, senior consultant at DNV.

Separately, classification society Bureau Veritas (BV) has approved a new wind-assisted 175,000 cbm LNG carrier design developed by China’s Dalian Shipbuilding Industry.

By Tuhin Roy

Please get in touch with comments or additional info to news@engine.online